Some shares could pay their own way in dividends alone, if those payouts are maintained at their current level. With a dividend yield of 9.8%, for example, if I bought British American Tobacco shares today I would have earned my purchase price back in little over a decade should the dividend stay flat – and I still own the shares. Many investors like the dividends offered by National Grid (LSE: NG) shares.

As the owner of a critical piece of national infrastructure that has no direct rival, National Grid may have what seems like a license to print money – and pay dividends.

In reality the picture is more nuanced.

Regulatory caps limit prices. Maintaining a large power distribution network can be costly.

But what if I had bought National Grid shares a decade ago? How would that investment have worked out for me?

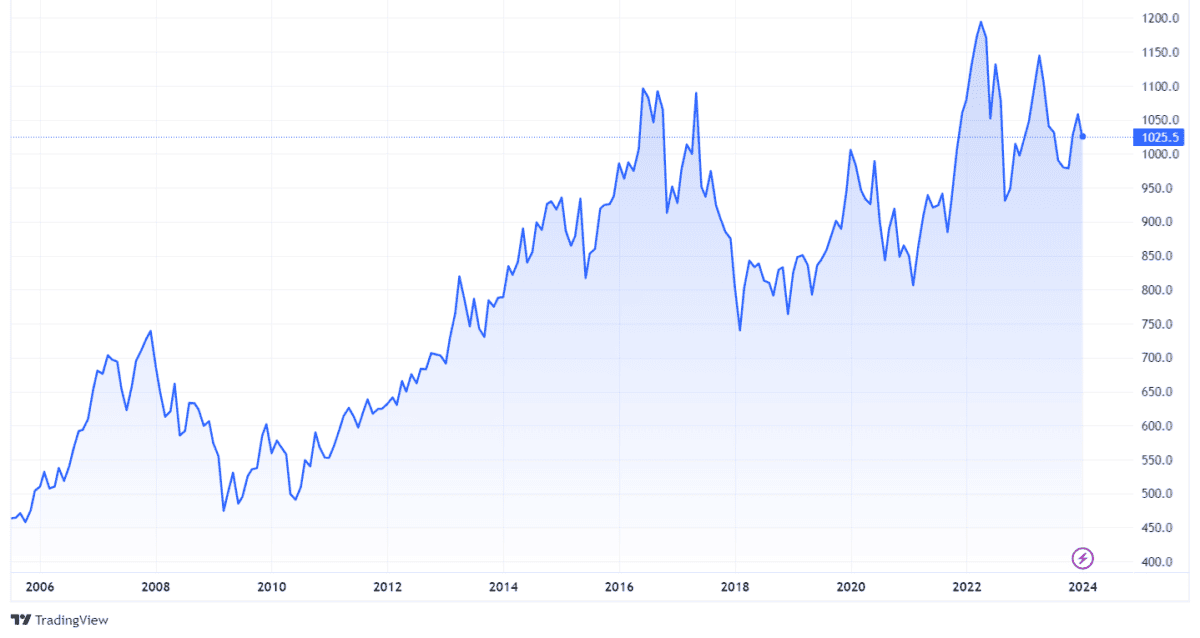

Positive share price change

A decade ago, National Grid shares were changing hands for just under £8 apiece. They are now trading for approximately £10.25 each.

In other words, my shares would now be worth 28% more than I paid for them 10 years ago.

Track record of ordinary dividend growth

As it happens, a decade ago today (22 January), National Grid paid an interim dividend of 14.5p per share. That compares to the latest interim dividend, paid earlier this month, of 19.4p per share.

But if I had bought back then, I would have missed the ex-dividend date already so my first dividend would have come in summer 2014.

During the period since then, the company has annually raised its ordinary dividends. On top of that, in June 2017, it paid a special dividend of 84.4p per share. That came after the company sold a majority stake in a UK gas distribution business. A share consolidation replaced each 12 existing shares with 11 new ones.

Excluding the special dividend, the shareholder distributions I would have received since buying the shares a decade ago would have added up to £4.75 per share. That does not cover my purchase price, but is equivalent to around three fifths of it.

Between share price growth and ordinary dividends, then, my holding would have given me a total return in 10 years approaching 90%.

Should I buy now?

Evidently, buying National Grid shares 10 years ago would have turned out to be a rewarding financial move for me.

What about now, though? After all, past performance is not necessarily an indicator of what might happen next.

The attractive features of the business are still in place, I reckon. It benefits from a network with no direct rival, with a large end user base and likely to benefit from resilient demand.

Yet over the past decade, net debt has ballooned. National Grid ended its 2013-14 financial year with £21.2bn of net debt on its balance sheet. By the end of March that figure was £41bn. The company expects it to increase by £3.5bn during its current financial year, when capex is expected to top £8bn.

Maintaining a national power distribution network and growing the dividend regularly is an expensive business.

In the long term, I do not think net debt can simply keep on rising indefinitely without the dividend being at risk. So I have no plans to buy National Grid shares today.