The Lloyds (LSE:LLOY) share price is down over 90% from its all-time high. While this might seem like an appealing time to make an investment, I’m not so sure.

Lloyds is famous as a banking group, and it dates back to 1765. It was one of the first banks in the world.

The share price saw its prime in the 1990s. Yet, since then, although the share price increased at moments, it generally headed downward.

The financial picture

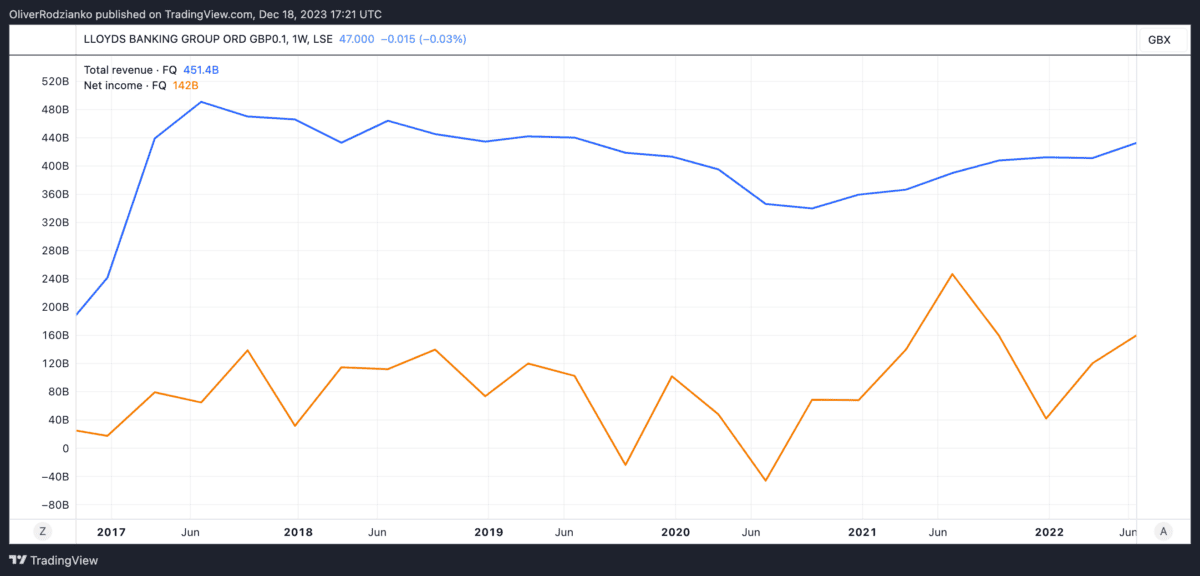

Interestingly, while total revenue increased quite significantly from £17bn in 2016 to around £18.5bn in 2017, it’s dipped since due to the pandemic and was reported at £18bn in 2022.

Net income, on the other hand, was £2bn in 2016 but has risen to £5.5bn in 2022. That’s despite a significant hit from the pandemic around 2019, too.

To me, that’s a good sign in some ways. Although the company has struggled with revenue growth, its internal management has allowed for growing net income.

The company also has a dividend yield of 5.4%, which could be attractive if I were focused on a passive income.

However, I do think it’s important for me to be aware of how well the company is managing its debt. And Lloyds seems to have quite a lot of it.

For example, it has an equity-to-asset ratio of 0.05. What this means is that 95% of the company’s assets are balanced by debt.

That’s quite severe, in my opinion. Based on the facts, that’s is in the bottom 15% of 1,473 companies in the banking industry.

Understanding the value

It seems intuitive to me that the company’s price-to-earnings (P/E) ratio would be low right now. That’s because of the historically low share price. And my hunch was right, at the moment, the ratio is around five.

But comparing that to other banking shares is important to me. NatWest has a P/E ratio of around five, and Virgin Money UK has a P/E ratio of around 12. The worldwide banking average is a P/E ratio of nine.

Personally, I think the company is definitely cheap, but I worry that it deserves to be so. For that reason, I think it could be a value trap.

My take

I’m concerned that the company won’t be able to get its revenue growth back on track, so I’m definitely hesitant to buy the shares.

One of the reasons I don’t like buying value shares that aren’t great businesses is that sometimes they don’t live up to my expectations of rising to ‘fair value’.

‘Fair value’ is an estimate of what analysts think a company is worth based on future earnings, discounted back to present-day value.

I’d rather buy the shares of companies that have growth momentum, too. That way, I’m not just trading on price but also buying a great business, the Foolish way.

So, this one’s not even going on my watchlist.