We can generate a second income from many sources. Some of us might take on extra work, take part in online research, or investing in the buy-to-let market. However, from experience I believe the most time-efficient and financially rewarding avenue in investing in stocks and shares.

How does it work?

Starting to invest can be relatively straightforward. First, I need to set aside some money that I’m comfortable investing – this can be as little or as much as I want.

Next, I need to choose an investment platform or brokerage account to open and there are quite a few out there.

With this account, I can buy stocks, bonds, or other investments. However, I should consider a tax-free Stocks and Shares ISA in the UK, which allows me to invest up to £20,000 each year without paying capital gains tax or income tax on the returns I make.

Once the account is set up, I should research and choose the investments you want to buy based on my financial goals and risk tolerance. I could start with well-known companies or diversified funds, and gradually build my investment portfolio over time.

However, I need to remember at all times that investing involves risks. It’s essential to do my research or seek advice from a financial advisor to make informed decisions.

Finally, I must regularly review my investments and adjust my strategy as needed to stay on track of my financial objectives.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

Achieving success

Let’s imagine I’m starting with £25,000. That’s a strong savings account in the UK. And, as such, I’ll need to transfer that from a savings account into a Stocks & Shares ISA.

As noted, I’ll only be able to transfer £20,000 in the first year. The rest could go into a non-ISA account which could be transferred into the wrapper in the second year.

The problem is, that with £25,000 invested, even in the most dividend-heavy stocks, I could only realistically achieve £1,800 a year in passive income. And that’s with today’s inflated yields.

So I’m going to want to keep my money invested, maybe adding to it, until my portfolio reaches a size where it can generate my desired income. And this is where a compound returns strategy comes in — the process of reinvesting my returns annually to achieve exponential growth.

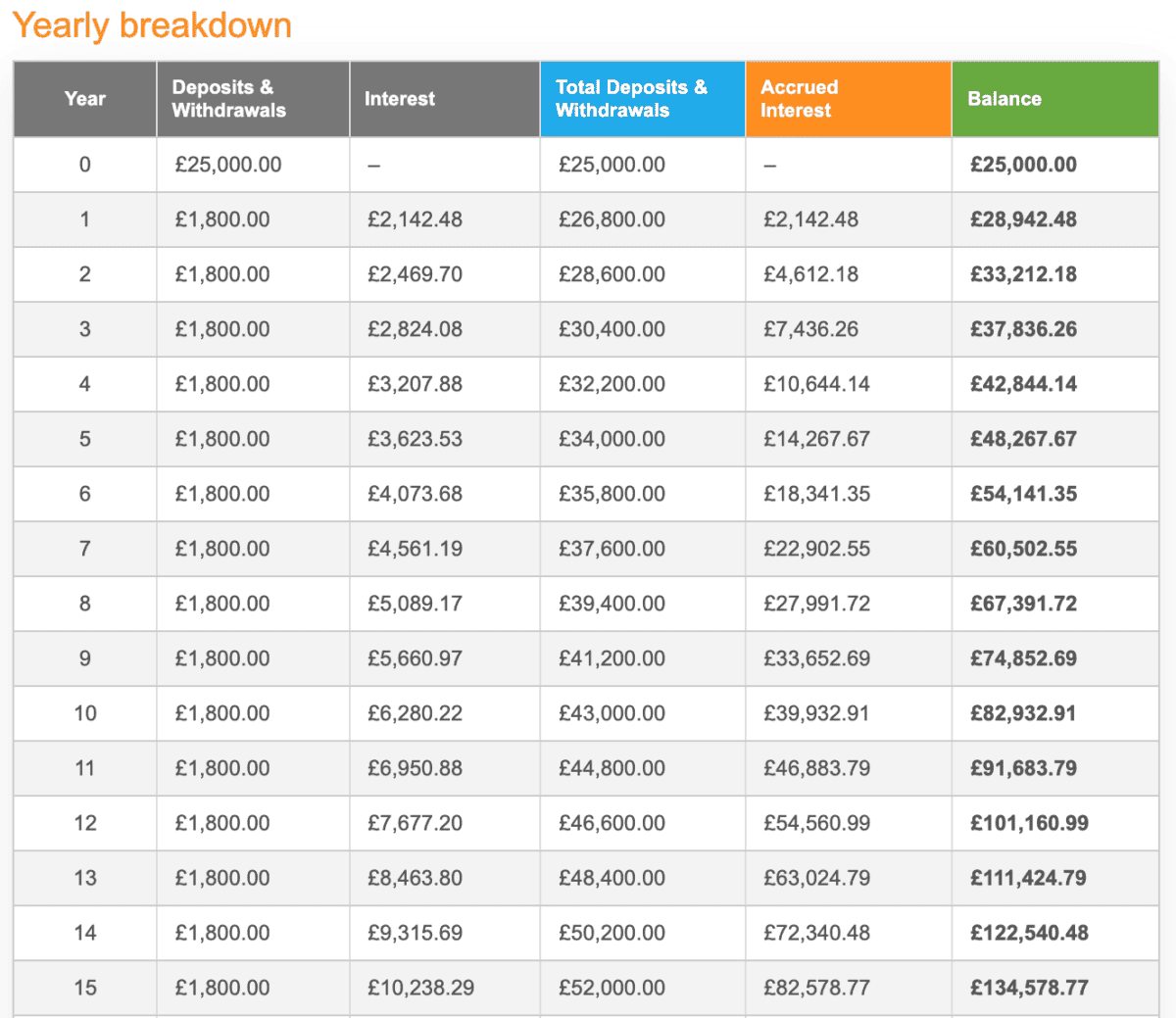

For example, if I invested my £25,000, achieving an annualised growth rate of 8%, while contributing a further £150 a month, after 15 years I’d have £135,000. That’s enough to generate £10,000 in passive income annually.

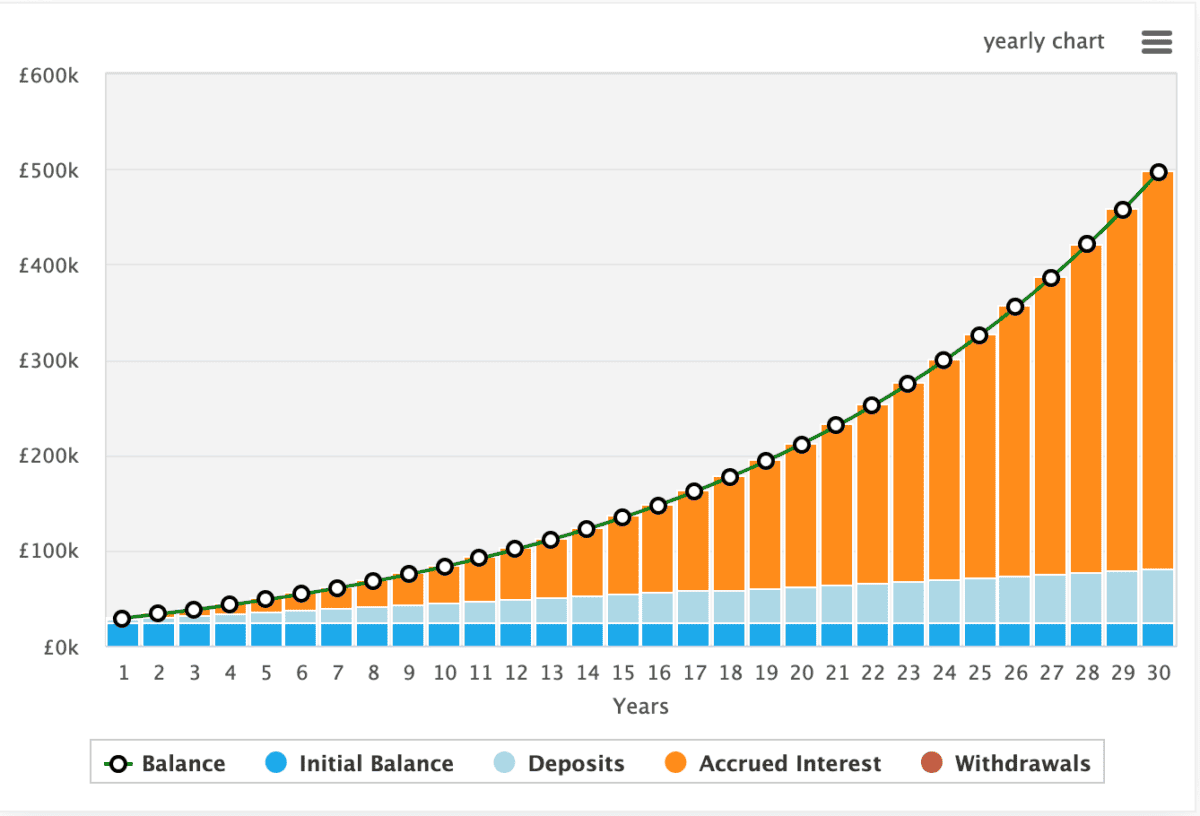

The above image highlights how the portfolio could grow. The chart below demonstrates the impact of compound returns. The thing with exponential growth rates is the longer I leave it, the faster it grows.

I’ve used 8% as an example, but better yields are certainly achievable. Seasoned investors often search for yields in excess of 10%. However, if I chose my stocks poorly, I could lose money.