Manchester United (NYSE:MANU) shares were making headlines again this week after the stock plummeted. The club’s shares fell by more than 18% in New York on Tuesday, 5 September.

The downward pressure on the shares was created by reports that the Glazer family had elected not to sell the club. If true, this would spell an end to the months of speculation that have driven the share price higher.

Media analysis

As is often the case, sports reporting and financial reporting rarely go hand in hand. And this was once again the case this week as I watched a rather botched attempted by the UK’s largest sports news show to analyse the situation.

The channel in question attempted to suggest that the peak share price, around $24, represented a huge discount versus the offers put forward by Sheikh Jassim of Qatar and British billionaire Sir Jim Ratcliffe.

Their maths being that the reported £5bn offered by Jassim was far above the $3.8bn share price. However, that’s not quite the case, as United has around £1bn in debt. Adding that the market price, the peak share price and reported bid also match up.

A buying opportunity?

The share price has since fallen to $19 on the reports that Glazer family would not be selling the club. According to the Mail on Sunday, Joel and Avram Glazer are holding out for an offer of £10bn.

When we take into account the aforementioned debt, the club, if valued at £10bn, would be worth around $55 a share. In turn, that represents a considerable upside from the current share price.

As a side note, the family bought Manchester United in 2005 for $790m. Manchester United has spent more than £1bn on interest and loan payments, plus share dividends — the majority of which have gone to the Glazer family — over the 18-year period.

Is £10bn feasible?

Manchester United might be among the biggest clubs in world football — if not the biggest — but $10bn represents a huge premium to any other previous club sales. My good friend Nicolas Moura recently published a white paper on the topic of private equity in football that dives deeper into these valuations.

To date, the largest buyout has been £2.6bn for Chelsea FC last year, followed by AC Milan at £1bn, and then AC Milan again at £680m. Further down the list we can see that Newcastle was bought by the Saudi PIF in 2021 for just £320m.

Long story short, there’s little precedent for a football club being worth $10bn. This is especially the case for a club that plays in a league where relegation remains a (distant) possibility as this can make a huge difference to risk, revenue, profitability, and valuation.

Likewise, Manchester United, as time has shown, are not guaranteed a place in the lucrative Champions League year after year. In fact, competition for that top-four place in the Premier League is becoming increasingly strong.

Personally, I don’t believe £10bn is on the cards, but there could be some upside from the current levels.

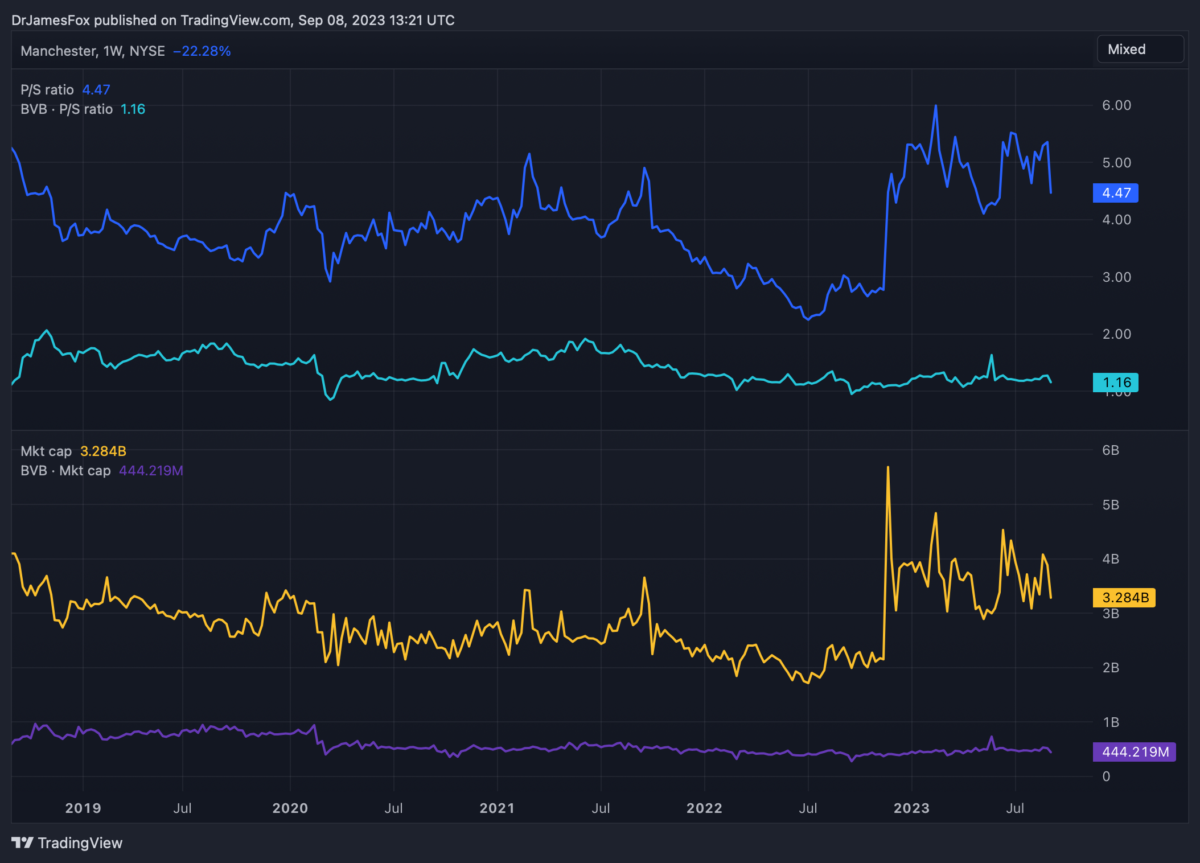

Finally, as an interesting comparison, here’s how United’s value compares to one of the other few listed football clubs, Borussia Dortmund. It’s worth remembering that Germany’s ’50+1′ regulation means German sides cannot be majority-owned by independent parties.