Investing in an index tracker that pay dividends is an easy way to generate a steady passive income. There is always the potential for decent capital growth as well.

One of the most popular of these trackers in the UK is the Vanguard FTSE 100 Index Unit Trust (LSE: VUKE). This ETF can be bought and sold just like any other regular stock.

But how much could it pay me in dividends if I invested £10,000 in it today?

What’s in it?

First, before looking at the potential income, here are the top 10 holdings, as at 30 April.

| % of fund | |

| AstraZeneca | 8.5% |

| Shell | 8.4% |

| HSBC Holdings | 5.7% |

| Unilever | 5.5% |

| BP | 4.6% |

| Diageo | 3.9% |

| British American Tobacco | 3.2% |

| Glencore | 2.9% |

| GSK | 2.8% |

| Rio Tinto | 2.7% |

One of the things I immediately like about this list is its diversity. There are well-established miners, giants in energy and pharmaceuticals, and diversified consumer staples companies here.

Yes, one possible criticism is that it doesn’t provide much technology exposure — but then tech stocks aren’t known for paying generous dividends.

This ETF currently yields 3.84%. That means I’d expect £384 annually from a £10,000 investment.

While no dividends are ever totally guaranteed, the payment here is sourced from all the Footsie’s dividend-paying stocks. In theory, that should make the income safer, particularly as most of the constituent companies sell products and services right across the globe.

Less appealing

Now, obviously central banks have been aggressively increasing base interest rates to try and tame stubbornly high inflation. As a result, investors can find higher yields elsewhere today.

For example, the UK 10-year gilt (a fixed-interest bond issued by the Treasury) is currently yielding 4.26%. So a 3.8% cash yield doesn’t sound particularly impressive in comparison.

So why should I bother?

Well, investing in a FTSE 100 tracker could also generate additional returns through share price appreciation. However, this isn’t guaranteed, as we can see by the fund’s poor -2.75% five-year return (excluding dividends).

Different paths

I think there are two alternative strategies investors could pursue here.

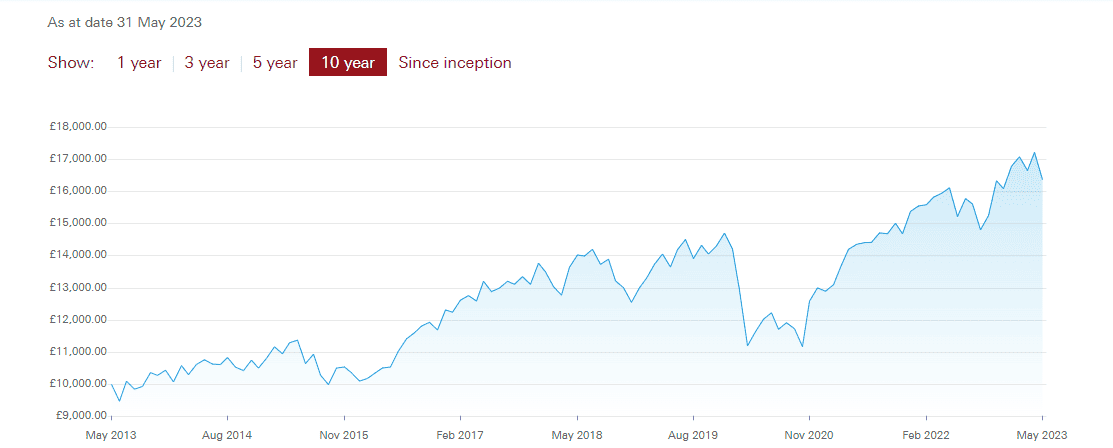

The first is buying a FTSE 100 tracker than reinvests the dividend payments back into the fund rather than paying them out. This tends to generate far superior returns, as can be seen below.

A £10,000 investment made a decade ago would now be worth over £16,000 as a result of reinvested dividends.

Of course, the drawback here would be the sacrifice of passive income today for potentially greater returns in the future.

Therefore, a second strategy could be to target those individual FTSE 100 dividend stocks that pay far higher yields than the average. And currently there are a good few of these in the Footsie.

One is investment management firm M&G, which currently yields a massive 9.6%. Meanwhile, British American Tobacco and Lloyds are yielding 8.6% and 5.3%, respectively. And insurance groups Phoenix and Legal & General both have cash yields above 8%.

So, if I spread my £10,000 between ultra-high-yield stocks such as these, then my portfolio could be generating passive income far above what I could achieve through bonds or index trackers.