Investing in banks can expose investors to huge amounts of risks. The recent collapse of Silicon Valley Bank (SVB) serves as a stark reminder of how fragile these institutions can be. So, here are three of Warren Buffett’s best tips on how to pick the best bank stocks.

1. Demand a margin of safety

Banking is inherently a risky business. High street banks tend to loan out sizeable chunks of customer deposits and earn profits from the interest they get from those loans. This means that they’re almost always in a deficit.

Thus, if customers begin to withdraw their funds en masse, banks may find it difficult to find liquidity, leading to what many refer to as a liquidity crisis. This was what led to the failures of SVB and several of its regional competitors.

Nonetheless, these failures were partially a result of irresponsible capital allocation. As such, Warren Buffett’s advice on finding banks with a margin of safety is extremely important. The Oracle of Omaha believes that buying a stock is like buying a business, and doing due diligence is essential.

Therefore, it’s crucial to ensure that a company has ample liquidity and a robust set of financials to withstand an economic downturn or liquidity crisis. These can be evaluated through ratios such as CET1 (comparing a bank’s capital against its assets), liquidity coverage, and countercyclical ratios.

2. Look for economic moats

Most of Warren Buffett’s investments are in conglomerates with competitive advantages over their competitors. That’s because companies that can successfully fend off competitors have better odds of growing their intrinsic value over time. This same precedent can be applied to banks.

The fall of several regional banks in the US has resulted in a flight to quality. Consequently, the likes of JP Morgan and Bank of America have received tens of billions in customer deposits since SVB’s turmoil. This is what Warren Buffett would call en economic moat.

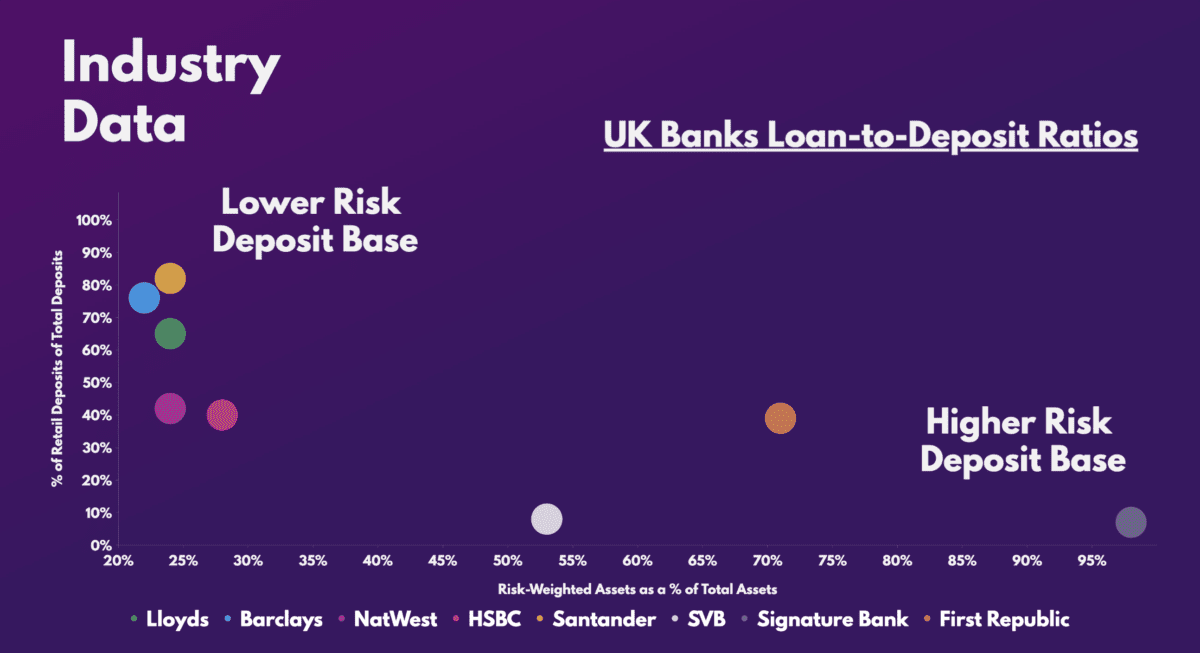

It’s for those reasons that UK banks stand out as the most attractive to me — their strength and reliability. This is because their lower-risk deposit base gives them a much bigger buffer to protect themselves from a liquidity crisis.

This stems from the fact that the amount of risk-weighted assets they hold are much lower than their US counterparts. Moreover, the number of retail customers they have is significantly higher. Hence, the likelihood of a bank run is lower as the majority of their funds are insured by a regulatory body.

3. Focus on the long term

Another Warren Buffett tip is to focus on the returns a bank can make over the long term. In the context of bank stocks, they should generate high interest margins (the difference between income generated from interest-bearing assets and liabilities) and good returns on tangible equity (ROTE).

Nevertheless, there’s a fine line between striving for large returns and potentially plunging a business into the ground. Getting too greedy can result in bankers taking unnecessary risks, while being too conservative may result in low profits.

Thankfully though, UK banks sit between the two, which is why I’m invested in Lloyds. And given their cheap valuation multiples with a strong outlook for net interest income and ROTE for the years ahead, I may even start a position in Barclays.

| Metrics | Lloyds | Barclays | Industry average |

|---|---|---|---|

| Price-to-book (P/B) ratio | 0.7 | 0.3 | 0.7 |

| Price-to-earnings (P/E) ratio | 6.2 | 4.5 | 8.9 |

| Forward price-to-earnings (FP/E) ratio | 6.6 | 4.7 | 5.7 |