The recent collapse of Silicon Valley Bank (SVB) has sent shockwaves throughout the banking industry. Consequently, bank stocks across the US and Europe have suffered double-digit drops over the past week. Nonetheless, here’s why FTSE bank shares could stand to gain from the downturn.

Why are UK lenders affected?

When a bank as big as SVB fails, others tend to follow. The great financial crisis is a stark reminder of that and how dominos can fall quickly. The failure of SVB has led to the collapse of other regional peers such as Silvergate Capital and Signature Bank, with First Republic Bank also now at risk.

Hence, it’s not uncommon to see bank runs occurring and liquidity crises springing up during times like these. Investors have been cashing out of FTSE bank stocks over the past week in fear of a contagion event. The recent news surrounding Credit Suisse‘s potential collapse hasn’t helped sentiment either.

How can they benefit from this?

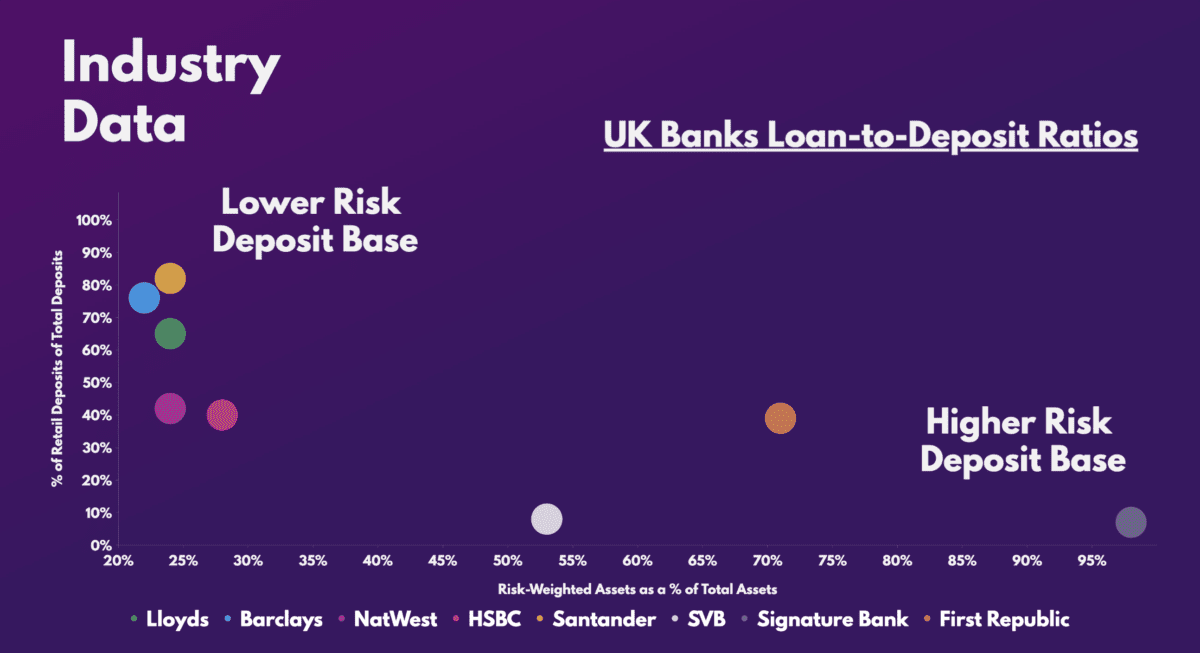

With customers withdrawing their funds en masse from digital banks, they’re going to have to deposit their money elsewhere. This is where the FTSE’s big banks stand to benefit, as the likes of Lloyds, Barclays, HSBC, NatWest, Santander, and its rivals are all seen to be safer alternatives.

UK lenders are known for having lower-risk deposit bases. That’s because the amount of risk-weighted assets they hold aren’t as high as their US counterparts. Additionally, a higher percentage of their clients are retail customers. This means that a liquidity crisis is less likely to unfold in the event of a bank run.

As such, I expect FTSE 100 banks to benefit if the banking crisis spreads to the UK. After all, JP Morgan and Bank of America have received a swamp of deposits as customers rush to place their funds in more secure banks, especially after ratings agency Moody’s cautioned against regional banks.

In fact, Barclays has already said that it’s seeing an increase in enquiries from its customers to switch or open business accounts in the past few days.

Should I buy FTSE bank shares?

It should go without saying that investing in financial firms can be a risky affair, as they can go under. Nevertheless, FTSE bank stocks are still worth a shout given their unique risk-reward proposition.

The decline of the Footsie in recent days has made an already cheap sector even cheaper. The index is renowned for its cheap valuation multiples, and there certainly are some bargains out there.

| Metrics | Lloyds | Barclays | NatWest | HSBC | Santander | Industry average |

|---|---|---|---|---|---|---|

| Price-to-book (P/B) ratio | 0.7 | 0.3 | 0.7 | 0.7 | 0.6 | 0.7 |

| Price-to-earnings (P/E) ratio | 6.2 | 4.5 | 7.0 | 9.0 | 5.9 | 8.9 |

| Forward price-to-earnings (FP/E) ratio | 6.6 | 4.7 | 6.0 | 5.5 | 5.8 | 5.7 |

So, given that most of them are trading on lucrative multiples, I’m considering expanding my position in Lloyds and potentially even starting one with Barclays, which looks to be the cheapest in its sector. As Warren Buffett once said, “be greedy when others are fearful, and fearful when others are greedy”.