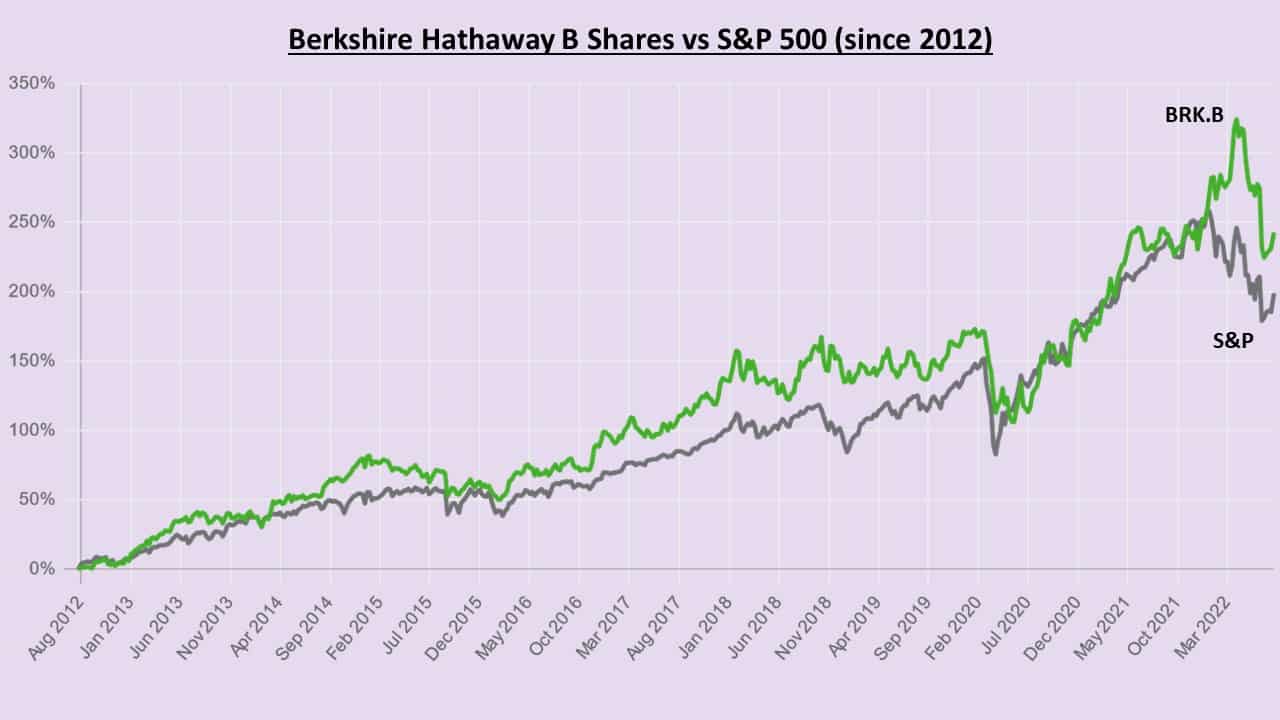

Investing conditions have been exceptionally tricky in 2022 for a variety of macroeconomic reasons. During this period of stock market volatility I’ve sought the teachings of experts like legendary investor Warren Buffett.

Buffett has made billions of dollars with his Berkshire Hathaway firm by buying shares when stock markets fall. His approach centres on finding value in falling stocks and watching them rise over the long term.

Stock markets have rallied in more recent days. But the multiple challenges facing the global economy — and the fragile state of investor confidence — means another Buffett-style buy-on-the-dip opportunity could be just around the corner.

2 Buffett-like stocks I’ve bought

When picking which shares to buy, Buffett looks for companies with strong ‘economic moats.’ This term is used to describe an advantage that a business has over competitors. Such moats can enable a company to keep growing its market share and profits over the long term.

With this in mind here are two UK stocks with economic moats I think Buffett might love.

Games Workshop

Economic moat: market-leading products

The fantasy wargaming sector is huge and growing rapidly across the world. And thanks to its Warhammer 40,000 game format which launched in 1987, Games Workshop (LSE: GAW) sits at the top of the industry.

Revenues at the business soared to record highs above £350m in the last financial year as its fanbase continued to grow.

Games Workshop’s Warhammer Age of Sigmar game is also growing rapidly following its launch in 2015. And the business is seeking to supercharge royalty income by licencing its intellectual property to other media, like video games.

The company could see revenues growth weaken as consumer spending comes under pressure in key regions. But niche product makers and retailers like Games Workshop could weather the storm better than those who sell mainstream goods.

Spire Healthcare

Economic moat: barriers to entry

I’ve bought Games Workshop shares for my portfolio. And I’ve also invested in Spire Healthcare (LSE: SPI) because of soaring demand for private healthcare. That’s despite the problem of rising labour costs to the company.

This Buffett-like stock operates almost 40 hospitals and several clinics in the United Kingdom. It takes vast amounts of capital to build and staff healthcare facilities like this. This is something which bars competitors from easily setting up and eating into Spire’s market share.

As I say, the number of private healthcare patients is booming right now. And as an investor in the sector I stand to make a lot of cash. Research shows that 69,000 people self-funded their medical treatment in the final three months of 2021.

This was up 39% from pre-pandemic levels. And this is in addition to the soaring number of people who are obtaining treatment through medical insurance. I expect patient numbers at the likes to Spire to keep surging as NHS waiting lists rapidly grow.