The Royal Mail (LSE: RMG) share price has seen a drop of over 40% since its pandemic high. The pandemic had initially kept everyone at home, spurring an unprecedented demand for home deliveries. But since restrictions were lifted, overall parcel volume has seen a decline. Nonetheless, I think there are some key factors that could send the share price on a rebound. The FTSE 250 firm will be reporting its full-year results next week. If results and guidance are positive, it could prove to be a turning point for the stock.

Pandemic care package

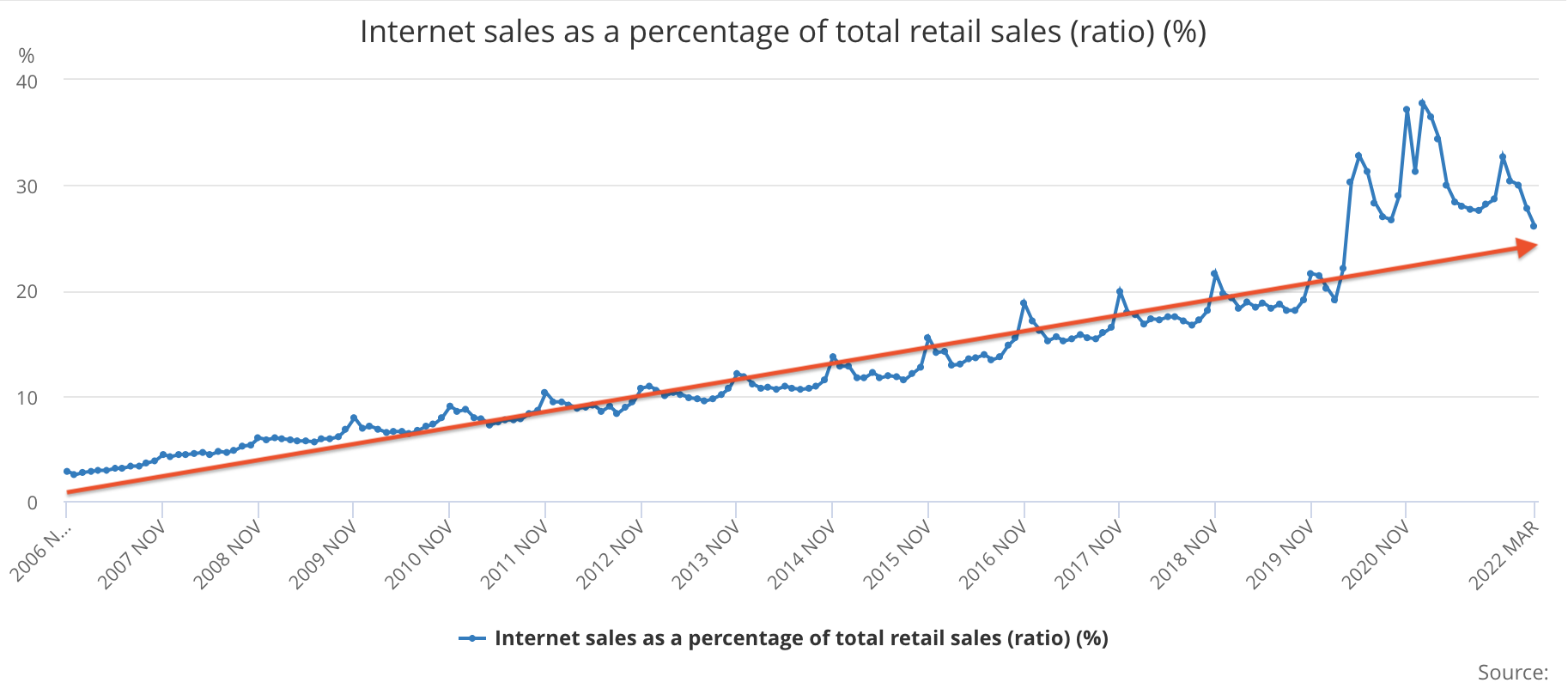

Given that the majority of the firm’s earnings stem from package deliveries as a result of online retail sales, the decline in overall parcel volume has hit its top line. Nevertheless, there is a silver lining — total parcel volume remains higher than pre-pandemic levels.

| Royal Mail Metrics for Q3 | 2021 | 2020 | 2019 |

|---|---|---|---|

| Parcel Volume (ex. GLS) | 439m | 496m | 382m |

| Revenue (£m) | 2,420 | 2,568 | 2,204 |

| Group Revenue (£m) | 3,554 | 3,641 | 3,035 |

The latest ONS data, reporting internet sales as a percentage of total retail sales, still indicates a long-term positive trend. This means Royal Mail has the potential to eventually rebound to its 2020 figures.

GLS flies higher

GLS is Royal Mail’s international arm. Compared to Royal Mail, it has a much bigger exposure to Europe and North America. In fact, GLS has done exceptionally better than its parent, growing parcel volumes and revenue by 34% and 35% respectively, as compared to 2019!

| GLS Metrics for Q3 | 2021 | 2020 | 2019 |

|---|---|---|---|

| Parcel volume | 239m | 228m | 179m |

| Revenue (£m) | 1,139 | 1,090 | 842 |

Although GLS’ revenue is no where near that of Royal Mail’s, the international business is still expected to post healthy growth levels. GLS acquired Rosenau Transport in Canada last year, and the effects of the takeover have shown to be positive.

Can Royal Mail deliver?

All this comes down to whether Royal Mail can deliver the goods. Guidance provided in its Q3 trading update was largely mixed. At that time, the impact of Omicron meant the outlook for the group was unclear. As such, guidance for operating profit in FY22 was £430m. The winding down of test kits being shipped will undoubtedly hit revenue, so that’s something to look out for. On the flip side, GLS is expected to grow its operating margin by 8%.

So, can the Royal Mail share price rebound? Possibly, but not in the short term, in my opinion. Recent UK retail sales figures have shown that consumer spending has taken a hit over the last couple of months. As the Bank of England continues to raise interest rates, borrowing and spending are expected to cool as well. Then there’s also the uncertainty surrounding how much of a hit Royal Mail’s revenue will take from the decline in Covid testing.

That being said, Q4 is usually a strong quarter for internet sales, so Royal Mail could gain from that. I believe that management will have to report incredible figures and margins for the stock to rebound. However, if the firm’s outlook sours, the stock could fall a long way. Given the risks associated with mediocre growth, I don’t think it’s worthwhile for me to buy Royal Mail shares.